Tax law and estate planning might bore you to death, but this brief tip could make a life-changing financial difference to your surviving spouse, and other loved ones, including disabled and chronically ill family or friends, as well any minor children in your life.

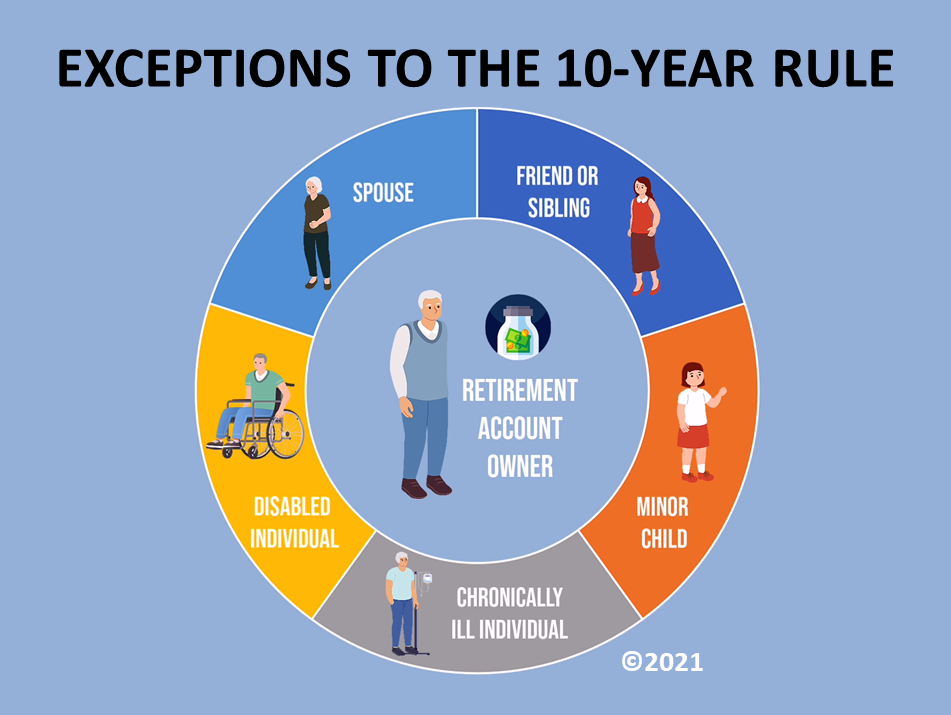

These individuals are among the five exceptions to the usual distribution rules on the inheritance of assets in IRA, 401(k), or other federally qualified retirement plans.

New rules, that went into effect on January 1st, 2020 with the enactment of The Secure Act, require the beneficiary of inherited IRA or 401(k) accounts to deplete the money in those accounts within 10 years. It was a technical change that many overlooked in the rush of tax law changes that occurred in 2020 during the pandemic. But it made a big difference in tax planning.

To be clear, until 2020, beneficiaries of an inherited IRA or 401(k) were not required to liquidate an inherited account within 10 years, as is now required, which had left open a major tax break: They had the option to stretch out distributions over their actuarial life expectancy, thus, leaving the assets to compound tax-free for a much longer period. The 10-year mandatory distribution rules carved out some key exceptions for certain individuals that now require attention, if you intend to pass on your retirement plan, IRA or other qualified plan assets to a spouse, chronically ill or disabled individual or minor child.

For a disabled individual, who inherits federally qualified retirement assets, for instance, stretching out distributions over decades could transform the inheritance into an income stream for life. The same is true for a widower, chronically ill individual, or minor child that inherits your retirement account.

In addition, a fifth exception to the usual distribution rules applies to a beneficiary that is less than 11 years younger than the retirement account owner. A sibling or friend who is 10 years or less your junior, who inherits qualified retirement account assets, also may use their life expectancy -- instead of taking required distributions over 10 years.

If you own a sizable IRA, 401(k) or other qualified account, and your beneficiary is your spouse, a friend or sibling 10 years or less younger, an individual with a disability, chronic illness, or a minor child, the five exceptions to the 10-year rule pose complicated tax planning as well as legal and investment issues requiring personal advice from a professional that is beyond the scope of this article.

This website uses cookies for navigation, content delivery and other functions. By using our website you agree that we can place cookies on your device. I understand