This is an unusual year-end tax planning season. The pace of federal tax law reform has increased in the four decades and accelerated since the pandemic.

In addition, tax simplification seems like a long-forgotten goal in recent tax reforms. For example, in February 2022, rules implementing the SECURE Act, which was signed into law December 2019, changed a highly technical part of the Internal Revenue Code affecting distributions from federally qualified retirement plans (QRPs) and IRAs, and it will change retirement funding and estate planning decisions for millions of Americans.

Meanwhile, stocks swung up and down this past summer and may stay volatile through the end of 2022, which creates opportunities to realize gains and offset them by taking losses.

To make things simpler, here are 20 reminders about ways to cut your federal tax bill by December 31, 2022. They’re for a broad audience of business owners, doctors, and employees in executive management as well as middle managers, teachers, and other hard-working Americans who are lifelong retirement investors.

1. Have you fully funded your IRA or 401(k) for 2022 to save for retirement and lower your tax bill?

2. If you expect to have a taxable estate in 2026, when the $12.06 million individual estate tax exclusion is slashed to $6.2 million ($12.4 million for married couples), consider making gifts to children and others by December 31.

3. If you expect to have a taxable estate after 2025, consider setting up a trust to transfer assets from your estate to reduce taxes, avoid probate, direct assets to be inherited on terms you specify, and provide your heirs protection from creditors, liens and divorce settlements.

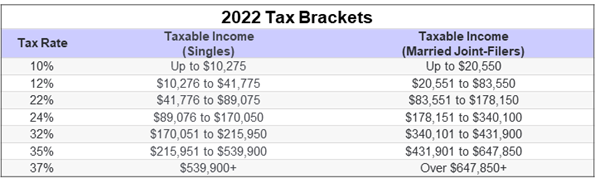

4. If you are edging into a higher tax bracket this year, have you considered ways of bunching charitable donations and other itemized deductions into 2022?

5. If you’re funding college tuition and other qualified education expenses, can you time tuition and other payments to bunch deductions and optimize your itemized deductions in 2022 or 2023?

6. If you own a traditional IRA, is this a good time to consider converting it to a Roth IRA, which could provide tax-free income and other tax benefits to your heirs?

7. If you experienced a financial loss from a property-casualty or theft or paid large property tax or medical bills in 2022, it may be deductible and may make you qualify to itemize deductions.

8. Consider donating appreciated assets to charity, such as publicly traded securities, real estate, or an interest in a private business, to lower capital gains taxes while helping the charity.

9. Have you cleaned out your garage, and other storage spaces to decide what you could give to charity that may have significant fair market value that can be written off against your taxable income with other itemized deductions?

10. If you’re planning to sell your business and have no buyer lined up yet, consider donating some of the proceeds from the sale to a charity to reduce gains taxes.